Required Minimum Distributions: Preparing for 2023

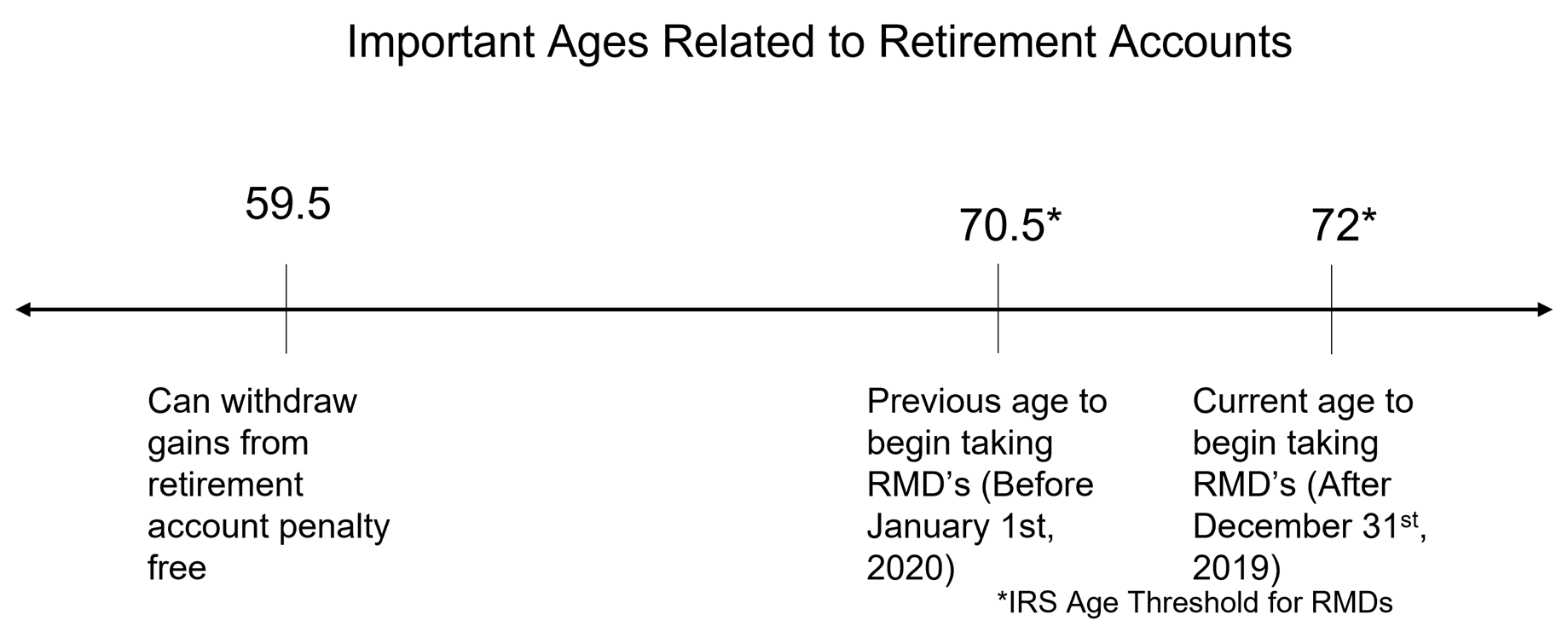

As we wind down towards the end of 2022, I’d like to discuss a complex topic that you should be prepared for in 2023: Required Minimum Distributions. The Required Minimum Distributions (RMD) is the amount of money you are required to distribute from your Individual Retirement Accounts (IRAs) or Employer-Sponsored Retirement Plans once you’ve reached a certain age. The IRS requires taxpayers to take these distributions to prevent them from using retirement accounts to avoid paying taxes. RMDs have different rules depending on the type of account. We highly recommended that you reach out to your financial advisor or tax professional for help in calculating your RMD to avoid any penalties.

The SECURE Act – In 2020, the IRS passed the Setting Every Community Up for Retirement Enhancement (SECURE) Act to mitigate the coming retirement savings crisis. One of the major changes was the required age to begin withdrawing your RMD increased from age 70 ½ to 72. A taxpayer must take their first RMD by April 1st following the year they turn 72, and then each subsequent year using the current RMD calculation. If you fail to take your RMD, the penalty is 50% of the remaining balance to be distributed! A RMDs calculation differs depending on the type of account, specifically if it is an inherited IRA.

While the SECURE Act had many benefits that resulted from its implementation, it took away a major estate-planning strategy called the Stretch IRA. The Stretch IRA allowed taxpayers to pass their IRA on from generation to generation, while taking advantage of the tax-free growth of the investments within it. Under the new rules, non-spouse beneficiaries who inherited an IRA after December 31st, 2019, will have to withdraw all the funds from the inherited account within 10 years of the death of the original account owner. Generally, if you inherited an IRA before January 1st, 2020, you can still calculate your RMD using the IRS Single Life Expectancy table.

2023 Outlook – Calculating your RMD can be a hectic process, especially if you have multiple retirement accounts and must take an RMD from each. You can always withdraw more than your RMD to be safe, but it may not be the best tax saving strategy. To ensure you take the correct amount and avoid all possible penalties, reach out to your financial advisor or tax professional to assist you in calculating your 2023 Required Minimum Distribution. Look for your 2023 RMD notices in January!